When it comes to protecting and growing your savings, fixed rate bonds are one of the most straightforward and reliable options available. For many UK savers, the best 1 year fixed rate bond offers a perfect blend of safety, predictability, and competitive interest rates.

In this comprehensive guide, we’ll break down everything you need to know about 1 year fixed rate bonds—from the basics to advanced strategies to make the most of them. Whether you’re new to saving or a seasoned investor, this guide is designed to help you confidently choose the best option in 2025.

What Is a 1 Year Fixed Rate Bond?

A 1 year fixed rate bond is a type of savings account where you deposit a lump sum of money for a fixed term—usually 12 months—in exchange for a guaranteed interest rate. You cannot withdraw your money during the term, but in return, you benefit from a higher rate than many easy-access savings accounts.

It’s a low-risk, high-confidence way to earn more from your savings, especially in today’s volatile economic environment.

Why 1 Year? Why Not Longer or Shorter?

Choosing a 1 year term strikes the perfect balance for many savers. Here’s why:

- Short enough to stay flexible in uncertain markets

- Long enough to benefit from better interest rates than instant-access accounts

- Ideal for financial goals within a 12-month window (e.g. weddings, travel, home deposits)

A longer bond might lock your money away too long, while a shorter one might not provide worthwhile returns.

Benefits of a 1 Year Fixed Rate Bond

- ✅ Guaranteed interest – No surprises; you know exactly what you’ll earn.

- ✅ Low risk – Protected up to £85,000 per institution under FSCS.

- ✅ Encourages saving discipline – No access means less temptation to dip into savings.

- ✅ Higher rates than easy-access accounts – You’re rewarded for locking away your money.

Best 1 Year Fixed Rate Bonds in the UK – May 2025

We’ve researched the top-performing fixed bonds currently available in the UK. Here’s a breakdown of the best offers this month:

| Bank / Provider | AER (Annual Equivalent Rate) | Minimum Deposit | Monthly Interest Option | FSCS Protection |

| Zenith Bank | 4.35% | £1,000 | No | Yes |

| Aldermore | 4.26% | £1,000 | Yes | Yes |

| OakNorth Bank | 4.05% | £1,000 | Yes | Yes |

| Hampshire Trust Bank | 4.22% | £1,000 | No | Yes |

| United Trust Bank | 4.35% | £1,000 | Yes | Yes |

Note: Always confirm details with the provider before applying as rates may change.

How Does a 1 Year Fixed Rate Bond Work?

Here’s a simplified process of how your money grows in a fixed bond:

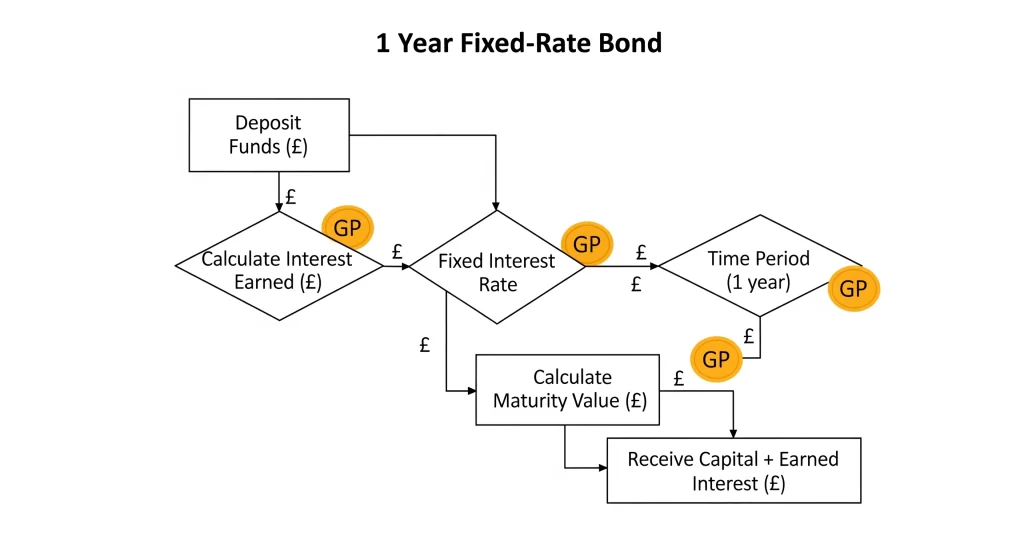

A 1-year fixed-rate bond is a type of investment where you lend money (in GBP) for a fixed period of 12 months, and in return, you receive a predetermined interest rate on your investment. The process is straightforward and offers a predictable return.

Here’s a simplified process of how your money grows in a 1-year fixed-rate bond:

First, you Deposit Funds (in GBP) into the bond. This is your initial investment, also known as the principal. Once you’ve deposited the funds, they become Funds Locked for 12 Months. During this period, you typically cannot access your money without incurring a penalty.

As the bond term progresses, Interest Accrues at a Fixed Rate. This means the interest rate was agreed upon when you opened the bond and will not change throughout the 12-month period. This provides a clear expectation of the returns (in GBP) you will earn.

After the 12-month period is complete, the Bond Matures After 1 Year. At this point, the term of the bond has ended.

Finally, you Receive Capital + Earned Interest. This means you get back your initial investment (the principal, in GBP) plus all the interest (in GBP) that has accrued over the 1-year term.

To help visualize this process, here’s the diagram for better understanding :

When you open a bond:

- You commit to a term—typically one year.

- You deposit your funds.

- The provider applies a fixed interest rate.

- At the end of the year, your deposit and the earned interest are paid back in full.

What to Look for in the Best 1 Year Fixed Rate Bond

1. Competitive Interest Rate

Look for the highest AER to maximise your return. Even a 0.10% difference can matter over larger deposits.

2. FSCS Protection

Always ensure the bank or provider is regulated by the Financial Conduct Authority and that your deposit is covered by the Financial Services Compensation Scheme (FSCS).

3. Flexibility on Interest Payments

Some bonds offer monthly or annual interest payouts—perfect if you want regular income instead of a lump sum at the end.

4. Minimum Deposit Requirements

Most providers require a minimum of £1,000 to open a fixed bond. Ensure it matches your available funds.

Tax Implications of Fixed Rate Bonds

While fixed bonds offer great returns, it’s important to understand the tax side:

- Interest from fixed bonds counts toward your Personal Savings Allowance (PSA).

- Basic rate taxpayers can earn up to £1,000 interest tax-free.

- Higher rate taxpayers get £500 tax-free.

- Additional rate taxpayers get no PSA.

If your total interest exceeds your PSA, you’ll need to declare it to HMRC and may owe income tax. For completely tax-free saving, consider a Fixed Rate Cash ISA, although rates tend to be slightly lower.

When Should You Consider a Fixed Rate Bond?

A fixed bond is a great option when:

- You have a lump sum you won’t need for the next 12 months.

- You want a risk-free return.

- You are saving for a specific short-term goal.

- You’re building a laddered investment strategy (more on this below).

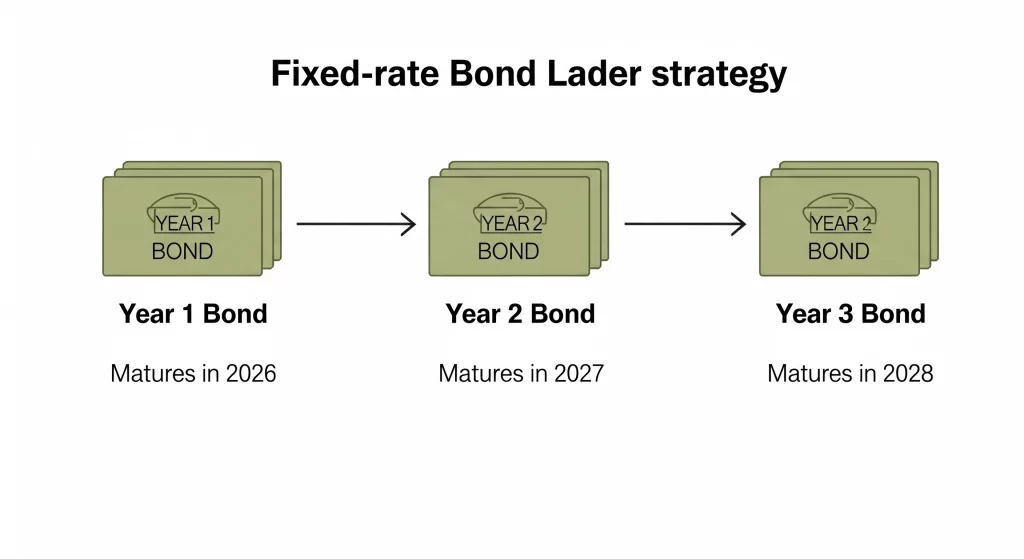

Advanced Strategy: The Fixed Rate Bond Ladder

This strategy involves staggering investments in bonds with different maturity dates. Based on the information you provided:

- A Year 1 Bond matures in 2026.

- A Year 2 Bond matures in 2027.

- A Year 3 Bond matures in 2028.

Here is a diagram illustrating this bond ladder:

This diagram shows:

- A ‘Year 1 Bond’ that ‘Matures in 2026’

- A ‘Year 2 Bond’ that ‘Matures in 2027’

- A ‘Year 3 Bond’ that ‘Matures in 2028’

This visual represents a bond ladder, where investments are spread across bonds with different maturity dates to potentially balance returns and access to funds.

Here’s how it works:

- You divide your savings into multiple 1, 2, and 3-year bonds.

- Each year, one bond matures and you reinvest it into a new 3-year bond at (hopefully) higher rates.

- This gives you annual liquidity while locking into higher long-term rates.

Step-by-Step: How to Open a 1 Year Fixed Rate Bond

- Research providers – Compare top rates and terms.

- Check eligibility – Ensure you meet age, residency, and minimum deposit requirements.

- Apply online – Most providers have quick digital applications.

- Transfer your deposit – Ensure the funds are sent before any rate deadline.

- Wait for maturity – Your money grows over the next 12 months.

- Review options at maturity – Reinvest, withdraw, or move to a new product.

FAQs – 1 Year Fixed Rate Bonds

Can I access my money before maturity?

Generally, no. Some providers allow early access with heavy penalties or loss of interest. Read terms carefully.

What happens at the end of the bond term?

The provider will return your initial deposit and the earned interest. Some will offer to automatically reinvest—opt out if you want to explore better options.

Can I open more than one bond?

Yes. You can spread your savings across different providers or stagger maturity dates using a bond ladder strategy.

Is it safe to open a fixed bond online?

Yes, as long as the provider is UK-regulated and FSCS-protected. Always verify before transferring funds.

Final Thoughts: Why Choose the Best 1 Year Fixed Rate Bond in 2025?

With the Bank of England base rate holding steady and inflation stabilising, 2025 is a golden opportunity for savers to lock in attractive interest rates without long-term commitments.

The best 1 year fixed rate bond gives you:

- A secure, predictable return

- Protection from market volatility

- Peace of mind with FSCS coverage

If you’re looking for a reliable way to make your money work harder while keeping risk to a minimum, a 1 year fixed rate bond should be at the top of your list.

Take action now. Review the latest rates, secure your bond, and start earning more on your savings today.

Disclaimer: The information provided on this webpage or post is for informational purposes only and should not be construed as financial advice. Any decisions made based on the content of this post are the sole responsibility of the user. We strongly recommend consulting with a qualified financial advisor before making any investment decisions. While we strive to provide accurate information, the content on this page may not always be up-to-date or fully comprehensive, and details such as interest rates and terms are subject to change without notice.”